On February 27 – the last trading day before fighting erupted in the Gulf – gold was up almost 60 percent from Chair Powell’s dovish Jackson Hole speech last August. The prevailing narrative for why this speech was such a catalyst is because this was the clearest signal yet the Fed would resume rate cuts, even with inflation significantly above target. Many took this to mean the Fed was downgrading its inflation mandate, perhaps due to relentless pressure from the White House to cut rates. In the months that followed, the rally in precious metals became known as the “debasement trade,” with gold seen as a safe haven asset amid mounting anxiety that high public debt levels will end up being inflated away.

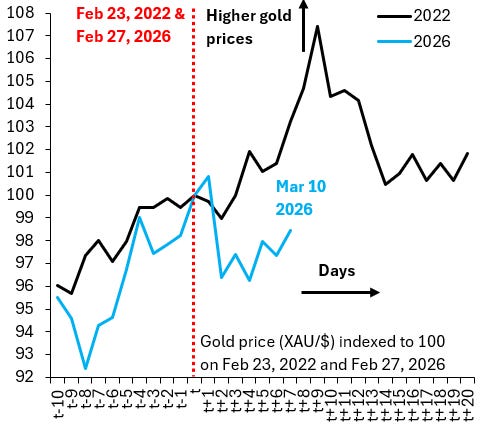

One of the interesting phenomena since the outbreak of hostilities is that gold hasn’t behaved like a safe haven asset at all. The chart above compares recent price action in the Bloomberg (XAU/$) gold price to that after Russia invaded Ukraine. In both cases, I’ve indexed the gold price to be 100 the day before fighting began, which is February 23, 2022, in the case of Ukraine and February 27, 2026, in the case of Iran. Gold rose modestly the first trading day after fighting in the Gulf erupted, but it then fell back and remains below where it was before war began. Has gold lost its safe haven status?

I don’t think so and see two reasons why recent price action has been “weird.” First, if you’re a safe haven asset, you need a meaningful risk-off event to rally. That just isn’t what’s been playing out in the S&P 500 since the start of hostilities. The chart above is the same format as my first chart and shows US stocks are barely down, even as oil prices looked like they might go through the roof at various points. Right or wrong, markets just don’t think war with Iran is all that scary. Second, the huge rise in gold prices over the past year – as the chart below shows – does have the potential to change how gold trades at key turning points. Unexpected shocks like war with Iran may cause people to sell assets that have risen a lot if they need short-term liquidity. This may explain some of gold’s recent underperformance.

The debasement trade is new and I don’t want to make it sound like I have any definitive clue as to why gold fell during the recent shock. My underlying view is that fiscal policy across most advanced economies remains just as irresponsible as ever, so the search for safe havens is real. The precious metals rally over the past year is just the beginning of a longer-lasting search for safe havens. Gold is just one manifestation of this and – in my opinion – will keep going higher.

Safe havens rarely behave like safe havens in the very short term.

In real shocks, investors often sell what they can, not what they want. Gold’s strong prior performance may have made it a source of liquidity rather than a source of protection.

The deeper issue still seems to be fiscal credibility and long-term monetary discipline. In that sense, the safe-haven debate is structural, not tactical.

If your leveraged into gold to ride the bull. Chances are you need to make margin calls when the missiles fly.

No posts