6 Comments

ITV News has just published an investigation: gambling company Sky Bet has migrated its business to Malta to avoid around £55m of tax each year. We provided technical support for the investigation, and this report goes into further detail of what precisely Sky Bet has done.

Sky Bet provides a vague explanation of why they moved to Malta (“a number of strategic and commercial reasons”), but this is untrue: they moved to Malta to avoid UK tax. This report sets out the details of what Sky Bet is doing, how much tax it will save, and whether (and how) HMRC should be trying to stop it. And we propose a way to reform gambling taxation so that businesses like Sky Bet no longer have an incentive to move offshore, and those that have moved offshore could have an incentive to return.

Sky Bet is a gaming company. It was part of Sky plc (the media group) but since 2018 has been owned by Flutter Entertainment, an Irish company that’s probably the world’s largest internet gambling business. The rights to the Sky Bet sporting business used to be held by a UK company, Hestview Limited.1

Looking at Hestview’s 2024 accounts, the company’s tax position looked broadly like this:

So Sky Bet’s total tax bill is about £136m (ignoring employee tax and second/third order effects).

Sky Bet’s owner, Flutter, at some point decided it wanted to reduce its tax bill – and this is why Hestview’s 2024 accounts say they decided to move to Malta:

But it looks like there was a last-minute change of mind.4 Instead of setting up a Maltese company, Sky Bet set up a UK company, SBG Sports Limited5, with a Maltese branch (this is clear from documents filed with the Maltese company registry).6

It’s not just a brass plate on an office building, but an actual headquarters, with its senior staff all physically now based in Malta.78

On the face of it, the total tax bill is now £107m. The relocation to Malta has saved at least £29m of tax.

That may, however, be just the start. Sources in the gaming industry tell us some people are going further and avoiding the VAT bill as well – and it’s being promoted by Maltese advisers.

Our hypothesis is that Sky Bet is doing something like this:

We asked Sky Bet specifically to confirm or deny that it was taking steps to eliminate its VAT charge; we received a generic statement which declined to comment on the specifics. It’s therefore our working assumption that Sky Bet is avoiding that £24m of Maltese VAT. On that basis, the relocation is now saving £55m or more of tax every year.

Our team of experienced advisers would not have advised a client to adopt this structure; it is aggressive and likely susceptible to both HMRC challenge and/or change of law. The following sections consider how such challenges and changes could be made.

The starting point is that, under current law, if a business genuinely relocates to another country then it no longer pays UK tax on its profits.15

There are, however, important points of detail that we would expect HMRC to consider:

Which is a long way of saying that a genuine relocation to Malta which still pays arm’s length (and probably very high) IP royalties to Hestview in the UK will be hard for HMRC to challenge – but such a structure would also present only limited tax savings for Sky Bet. A structure which aggressively tries to minimise the royalties paid to the UK would be more financially attractive for Sky Bet – but greatly increases the prospect of a successful challenge.

It’s important to note that we do not know if Sky Bet is using the VAT avoidance structure outlined above – this is our speculation (which Sky Bet pointedly did not deny). However we are reasonably certain that at least one other group is currently using a structure of this kind.

The EU and UK VAT systems are not supposed to enable businesses to magically make their VAT cost disappear. It is entirely proper for the UK to find any way it can to block this kind of structuring, either under current law or by changing the law.

Under current law, we’d expect HMRC to investigate whether the advertising services supplied to entities like ServiceCo are really being supplied to Belgium/Luxembourg/Ireland, or to a “fixed establishment” in the UK. This again will in large part come down to how carefully the structure is implemented.

Recent history has been that HMRC has failed to successfully challenge this kind of avoidance. VAT is a creation of EU law, and EU law has only enabled tax authorities to attack the most highly artificial types of VAT avoidance. So, for example, the UK Government passed legislation in 2019 aimed at stopping “offshore looping” by insurance brokers – routing arrangements through an offshore company to avoid VAT. That’s fairly close to the structuring we believe Sky Bet may have used. A tax tribunal recently held in the Hastings case that the 2019 legislation was contrary to EU law, resulting in a £16m VAT refund for Hastings.21

The upshot is that, as one adviser told us – “VAT avoidance is okay even if ‘blatant’ – as long as you do it right”. This should change. There’s no reason, post-Brexit, that UK VAT rules should accept that “blatant” VAT avoidance is “okay”. The Government should legislate:

It is common for reporting on corporate tax avoidance to say that there is no suggestion that tax planning is unlawful. That is not necessarily the case here.

There appears to have been an element of concealment in how Sky Bet/Flutter has described the arrangement. The public version is that the relocation to Malta is being executed for “strategic reasons” (and more on that below). However, ITV’s source at Flutter is clear that the real reason was tax:

“Tax was the elephant in the room. It was absolutely understood, across everyone affected, indirectly affected or even aware of it… that this was about tax.“

Our industry sources, and our panel of experienced tax experts, believe that this is likely correct.

If Sky Bet told HMRC that the arrangement wasn’t driven by tax, but it in fact was, then that was improper and potentially unlawful.

The current situation is irrational. It’s easy for a business providing gaming to UK consumers to move offshore, and save large amounts of corporation tax. That loses tax revenue; it also puts UK-based operators at a commercial disadvantage, giving them a large incentive to move offshore. This is not in the UK’s interest.22

It would be easy to reverse this: the Government could equalise all UK duties and tax for onshore and offshore businesses that provide internet/remote gaming services. There are two ways this could work.

Either approach would put an end to offshoring by internet gaming companies, and encourage relocation to the UK.2627

We asked Flutter, Sky Bet’s owners, for comment. They didn’t reply. They did send the following reply to ITV News:

“Flutter paid more than £700 million in taxes to HMRC last year and we employ over 5,000 people across the UK including almost 2,000 in Leeds and 600 in Sunderland.

As with most global businesses around the world, we are constantly striving to remain competitive and efficient and to give ourselves the best chance of success in an incredibly challenging environment.

The challenge we face is only made harder by the recent Gambling Act Review, the significant rise of illegal, unregulated black-market competitors and the possibility of tax rises in the Budget.

In June this year, after migrating Sky Bet onto the same technology platform as our other brands, we decided to move a number of commercial and marketing roles to our commercial centre in Malta – where Flutter already employs over 750 people.

This decision was made for a number of strategic and commercial reasons and will have some tax implications. But Flutter is committed to the UK and Sky Bet will continue to pay UK corporation tax on its profits.“

This is unconvincing. The new SBG Sports Limited was established in May 2025, long before the various Budget rumours started circulating. Any measures arising from the Gambling Act Review – new duties or regulation – will apply to gambling businesses with UK customers, regardless of where they are based.

So this adds to our sense that Sky Bet is hiding the true reason for its move.

Many thanks to Joel Hills at ITV – this story only exists because he spotted the Malta migration. And thanks to A O, K and M for their insights on the gaming industry and its tax treatment.

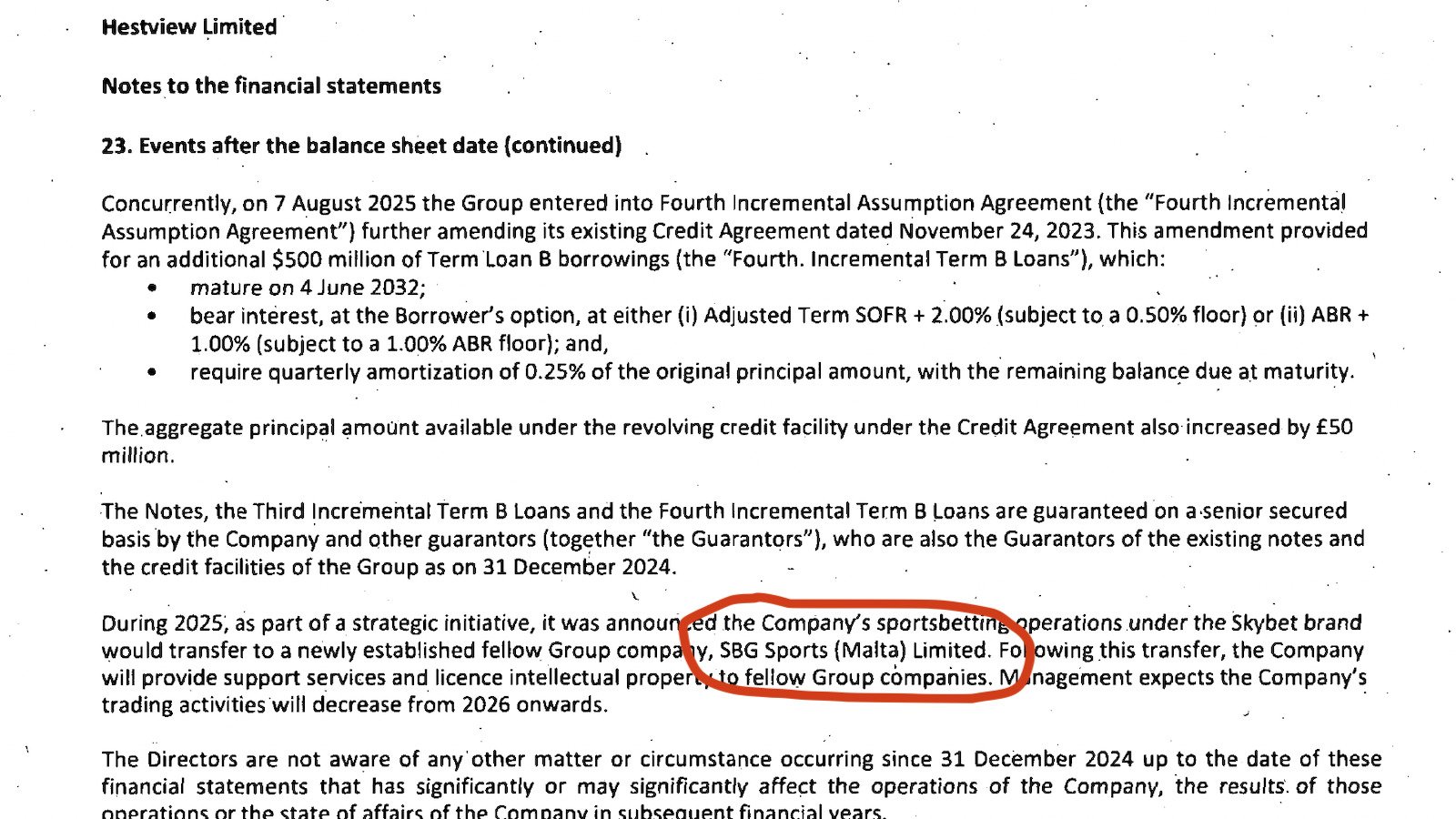

Historically, Hestview was the UK-licensed bookmaker in the group and the entity that licenced the “Sky Bet” brand from Sky plc. The accounts say Hestview was the “economic beneficiary of the Sky Bet brand”. It seems the position is now that SBG Sports Limited runs the sports betting business, Bonne Terre Ltd (a company incorporated in Alderney – part of Guernsey with particularly favourable gaming regulation) the egaming/casino business, and Hestview has retained “free to play” business. ↩︎

We are using round numbers throughout but they are representative of the actual figures. ↩︎

i.e. because sports betting is VAT exempt in the UK and so Sky Bet cannot recover the VAT. If this was (eg) a supermarket buying advertising then it would recover it. A further point of detail: if any advertisers were outside the UK then Sky Bet would “reverse charge” the VAT – so the UK Sky Bet business would always be subject to irrecoverable UK VAT on its marketing spend. ↩︎

Or possibly an error in the accounts, with someone writing “SBG Sports (Malta) Limited” instead of “SBG Sports Limited, Malta branch”. Either way, we can find no record of an “SBG Sports (Malta) Limited” in the UK, Malta, or anywhere else. ↩︎

“Sky Betting and Gaming” ↩︎

A branch isn’t a legal entity – it’s just a place where you operate. Banks often have branches because of the way bank regulation works (e.g. most of the world’s largest banks have branches in London). Some other regulated sectors do this too (insurance in certain cases). But outside of this kind of case, branches are unusual, and often a sign of tax/VAT avoidance. ↩︎

This is probably why they picked Malta rather than Alderney, even though Alderney tax and regulation is more straightforward (and in practice usually zero tax). You can’t realistically move dozens of employees to Alderney – the island is just too small. You wouldn’t be able to achieve the “substance” that is realistically required to escape UK corporation tax and VAT. ↩︎

Possibly the intention is that the company becomes Maltese tax resident. The UK/Malta double tax treaty has an old-fashioned “place of effective management” tie-breaker. Modern treaties have an anti-avoidance provision created by the OECD BEPS Project which means that tax authorities have to agree any shift in corporate residence. However our industry sources expected that wouldn’t be the planning here, and the entity was in fact intended to remain UK resident with a Maltese branch. More on the reasons for this below. ↩︎

Malta is not a normal country – only a few years ago, a journalist investigating corruption was murdered by a car bomb. The EU Commission shouldn’t permit Malta to engage in aggressive tax competition, like having a de facto 5% rate of corporate tax, and manipulating VAT grouping rules. However it seems unlikely we’ll see any action in the short term. ↩︎

Of course assuming profit is still £156m. ↩︎

In principle the tax benefit should be greatly limited by Pillar Two, the OECD 15% minimum tax. We’re still in the first few years of implementation, so it’s hard to say what is happening in practice here. One possibility is that Sky Bet really is paying 15% tax on its profits (in Ireland or some other jurisdiction); in that case VAT may be central to the structure. The other possibility is that a structure and/or accounting methodology is being used that minimises the impact of Pillar Two. We expect this kind of question will have answers in a few years, but for now all we have is intuition: and our intuition is that Sky Bet/Flutter are doing something to mitigate the 15%. ↩︎

On the basis it makes taxable supplies to SBG Sports Limited. ↩︎

This branch would solely be a tax play. ServiceCo has maybe a couple of people doing something that can be justified as a real activity (for example managing advertising for a particular (small) part of Sky Bet’s business). ↩︎

Malta has acted in a predatory way here, only permitting VAT groups for sectors where cross-border tax avoidance will be attractive, with advisers being fully aware that they can use this VAT grouping for avoidance purposes. The EU Commission clearly doesn’t like this, but thusfar hasn’t acted. ↩︎

There are numerous exceptions, of course, particularly if the business is ultimately owned by a UK individual or company, or if it holds UK real estate. However for a foreign-owned trading business, the general proposition is broadly correct. ↩︎

Which then makes the IP available to its Maltese branch. ↩︎

There are clear signs of that. Why use a branch rather than a Maltese company? One reason is – we would speculate – that it means that there’s no Maltese VAT on licence fee payments, because the IP is routed from Hestview Limited, via SBG Sports Limited’s UK headquarters to its Maltese branch. The UK companies would likely be VAT-grouped (so no VAT there). The arrangement between SBG Sports Limited in the UK and its Maltese branch would be an intra-entity transaction, and therefore not subject to VAT. It’s possible that the branch is also part of the direct tax planning. ↩︎

This is the opposite of the structuring used by many foreign companies with businesses in the UK, where they seek to maximise the licence fee paid by the UK operating business to the foreign owner of intellectual property. ↩︎

And there will be branch allocation issues unless SBG Sports Ltd is Maltese tax resident. However we wonder if the intention is in fact that the company remain UK tax resident. If they are careful about substance, the diverted profits tax (originally announced as a “Google tax“) wouldn’t then apply, because SBG Sports Ltd would be a UK company with a foreign branch, not a foreign resident company. ↩︎

And if it is intended to be Maltese tax resident, it may accidentally become UK tax resident. ↩︎

Hastings UK was making supplies (back office insurance related) to a non-EU insurer. Until 2019, these supplies were “specified”, meaning that there was VAT recovery, even though these services would be exempt in the UK. Hastings – and many others – took advantage of that by “looping” supplies to UK clients via non-EU entities, solely to achieve recovery. The law was changed in 2019 to stop these structures – recovery would only be permitted where the ultimate customer was outside the EU. The FTT decided in Hastings that EU law prevented UK VAT law from looking at the ultimate recipient of supplies. The “Offshore Looping Order” was held to be ultra vires because it wasn’t compatible with the Principal VAT Directive – the UK couldn’t restrict input tax recovery by looking through to the ultimate insured when the Directive didn’t. ↩︎

This is regardless of our position on whether we should encourage or suppress gaming generally; the question is whether the gaming industry that we do have should be onshore or offshore. ↩︎

It would only be the corporation tax on the gaming-duty-relevant profits that was creditable. ↩︎

The corporation tax figure is 25% x its 2024 profits (ignoring its deduction for gaming duty). The gaming duty figure is 19.6% of £580m, minus the £58m of corporation tax. ↩︎

It might be argued this breaches the UK’s double tax treaty with Malta. That is probably incorrect, because gaming duty is not a tax on profits. However the point is academic: even if gaming duty were (for some reason) regarded as a tax on profits, there’s no route to any appeal under UK tax law, because gaming duty is not one of the taxes which can be overridden by tax treaties. ↩︎

One side-effect of moving from corporation tax plus duties to pure duties is that operators with lower margins would pay a higher effective rate, and more efficient/higher-margin operators would be favoured. Given the essentially similarity of internet gaming businesses, this is significantly less problematic than it would be to (for example) tax digital companies on a gross revenue basis. ↩︎

An additional step that could be taken is to amend the diverted profits tax so section 86 applies to artificially structured foreign branches of UK companies. ↩︎

They may employ 5000 staff in the UK but that doesn’t account for the vast numbers they’ve made redundant https://www.racingpost.com/news/britain/around-220-jobs-under-threat-at-flutter-entertainment-as-company-begins-redundancy-consultation-avqYU8m3Fm0C/ and this move probably puts more of those jobs on rocky ground

Great article Dan.

Couple of additional thoughts as someone who used to advise in this space.

Whilst the Maltese gaming regulator is often cited as being much easier to work with than some others, I can almost guarantee that the move to a Maltese operator was VAT-driven. SkyBet is relatively unusual that it maintained such a significant presence in the UK for so long, as most of the other big players in the market have large Maltese establishments.

Its not just getting VAT-free marketing (through the branch structure you referenced) which is a driver towards Malta, although it is a significant element, as EU member states have the right under Article 135 of the VAT Directive to set the scope of their own gambling VAT exemptions.

Malta decided to make certain types of gambling (online slots, etc.) taxable in Malta. When supplied to non-Maltese customers this gives a right to VAT recovery but no requirement to pay any output tax. This right to recovery isn’t available in most other member states.

Malta also went further and exempted certain services which are essential to the provision of VAT exempt gambling (these are referred to as white-listed services in the industry). This means that some of SkyBet’s key inputs will now become exempt too, lowering its irrecoverable VAT base.

I’m not fully aligned with your view on how aggressive the use of Malta’s whole entity VAT-grouping regime is. The Skandia/Danske Bank decisions of the CJEU (which require a shift to Swedish-style establishment only VAT grouping) still haven’t been adopted in other significant jurisdictions such as Ireland and Germany. The UK also maintains this approach to VAT grouping. There are also many other valid commercial reasons to maintain a branch structure (as is common in various financial services sectors), albeit in the gaming sector they tend to be tax-driven.

A key distinction however is that places like the UK have implemented anti-avoidance provisions (s43(2A)) to prevent the sort of mischief that your article refers to. Malta has chosen not to implement such provisions, presumably to support the massive hub of gambling businesses setting up shop there.

many thanks, Rat!

We initially thought the taxable/recoverability rules in Malta would be the key, but the business that’s moved only does sporting betting, so it seems that’s not it. ServiceCo/VAT grouping most likely. I agree that the technical basis of the UK’s approach is the same. However there’s a big difference: the UK does it to facilitate fiscal neutrality within international groups; any attempt to use the grouping to avoid a reverse charge on what are (in reality) supplies from third parties is not permitted (s43(2A) as you say). For Malta, bona fide “within group” cases are unlikely given the nature of Malta’s economy. It’s all about enabling precisely the thing s43(2A) blocks. So it’s predatory!

Thorough and probably highly accurate analysis as always, Dan. A couple of minor quibbles. Branches are not that unusual – in low/zero tax jurisdictions, they may be a sign of tax avoidance, but in a number of industry sectors they are a way to access pan-EU regulatory regimes, for example. Also on your tax savings, the benefit will be (slightly) reduced by Pillar Two (I assume Flutter large enough to be in scope given the Sky Bet net stakes receipts you mention above)?

thanks – was at one point a footnote on Pillar 2 but it seems to have gone… will reinstate! It adds to the feeling that VAT is a big part of this.

And I should generalise the reference to banks as legit users of branches

Hi Tim

Agree that P2 is the missing part of the analysis, but the branch element is likely to be a key part of the tax driver here. Due to the asymmetry in the Permanent Establishment definitions in the model rules and transitional safe harbours, a branch can be a PE for one rule set, and not another. Cutting through what amounts to a 100 page memo, the effect is to drastically reduce P2 paid (though this does rely on there being some headroom in the Effective Tax Rate in UK for the group as a whole). This is a well known weakness in the TSHs and has been exploited by a number of MNEs.

Your email address will not be published.

Legal and privacy

© Tax Policy Associates Ltd, a non-profit company limited by guarantee, no. 14053878